India's IT services majors closed FY2025–26 with deal pipelines at record highs and revenues under pressure — as AI deflation began compressing the per-unit economics of the very services that built the industry's global standing

India's IT services industry entered fiscal 2025–26 carrying two contradictory truths. On one hand, India's total technology industry — covering IT services, BPM, engineering R&D, software products, hardware, and GCCs — was approaching the historic $ 300 billion revenue milestone that NASSCOM had long projected as a symbol of the sector's maturity and global standing. On the other, the very technology driving that growth — artificial intelligence — was beginning to deflate the per-unit economics of the IT services that had built the industry's scale. AI was automating testing, coding, documentation, and support functions that had historically been delivered by large teams of engineers. Revenue was growing, but headcount growth was slowing. Deal sizes were rising, but margins were under pressure. The IT services industry's FY2025–26 story is not a simple story of success or struggle — it is the story of an industry navigating both simultaneously, and the firms that navigated it best are those that moved fastest toward AI-first delivery.

The Industry in Numbers: Understanding the Scale

Before reading India's IT services market, it is important to understand what different figures measure — because the numbers reported by different bodies cover different scopes, and conflating them creates a misleading picture.

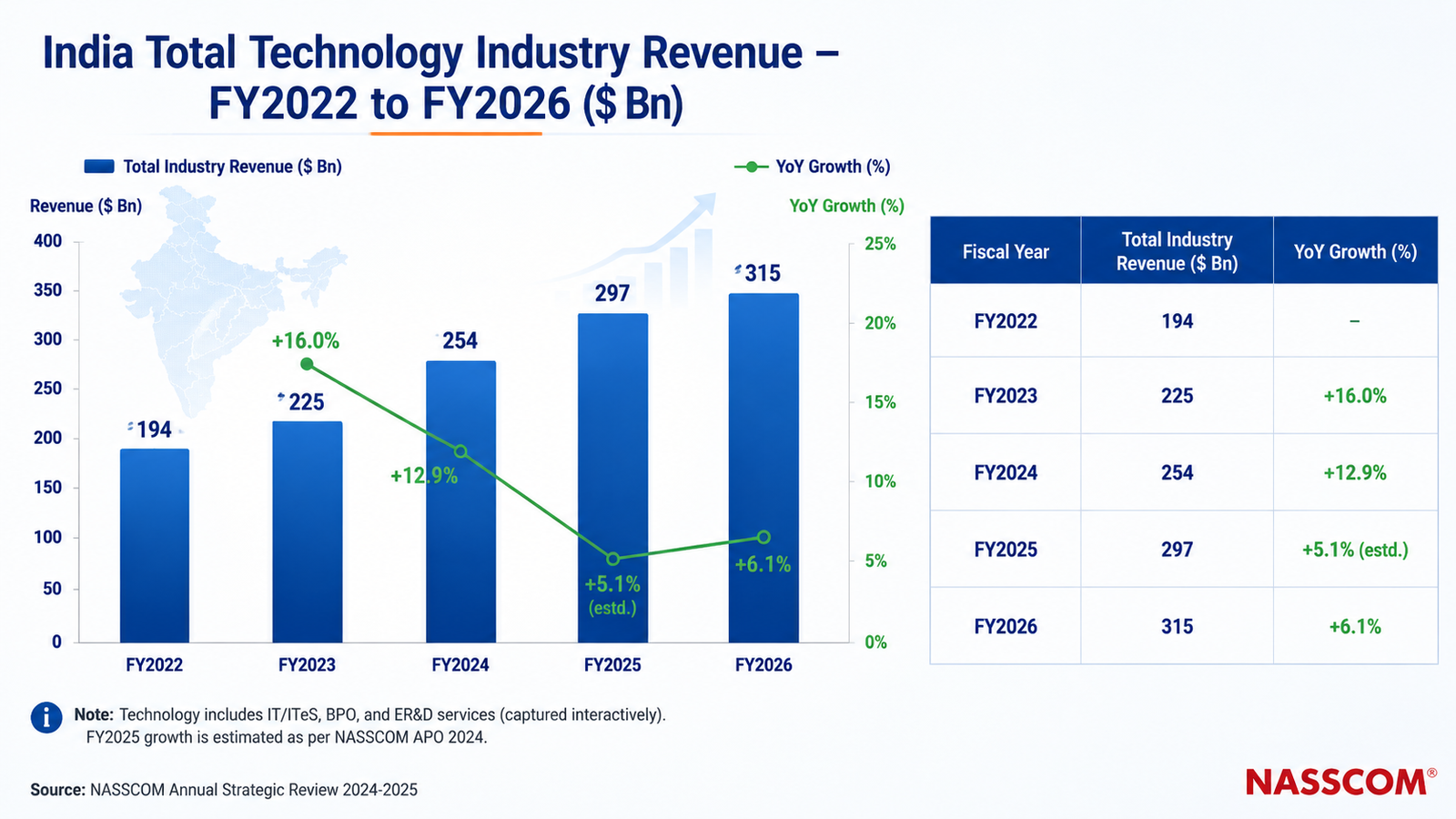

The broadest measure is the total Indian technology industry — which NASSCOM defines to include IT services, business process management, engineering R&D, software products, hardware, and the Global Capability Centre ecosystem combined. This total industry figure reached $ 315 billion in FY2025–26, up 6.1 percent year-on-year from the revised FY25 figure of $ 297 billion, according to NASSCOM's Annual Strategic Review 2026 published in February 2026. Total technology exports within this figure reached $ 246 billion in FY26, up from $ 224 billion in FY25.

Within that total, IT services exports are the largest single component. According to NASSCOM data cited by IBEF, IT services exports accounted for over 65 percent of India's total technology exports in FY25 — implying an IT services export contribution of approximately $ 145–150 billion in FY25, rising proportionally in FY26. The United States remained the dominant export destination at $ 103.2 billion — 54.1 percent of total exports — followed by Europe at $ 58.8 billion, or 30.8 percent.

A third and distinct measure is India's domestic IT services market — the market that serves Indian enterprise and government clients within the country. IDC's Worldwide Semi-annual Services Tracker placed this domestic IT and Business Services market at $ 16.5 billion in 2024, growing 6.9 percent YoY, according to IDC's July 2025 release. IDC projects this domestic market to grow at a CAGR of 12.3 percent through 2029.

Finally, the broadest spending measure is total IT spending in India — which covers all enterprise and government expenditure on IT hardware, software, and services within the country, regardless of whether the vendor is Indian or foreign. Gartner places this figure at $ 161.5 billion in 2025, growing to $ 176.3 billion in 2026 — driven by data centre expansion, AI-enabled software investments, and enterprise digital transformation.

These four measures — total technology industry revenue, IT services exports, domestic IT services market, and total IT spending — are complementary lenses on the same ecosystem, not competing claims. Each is valid for a different purpose, and this article draws on all four where relevant, with the source and scope clearly identified each time.

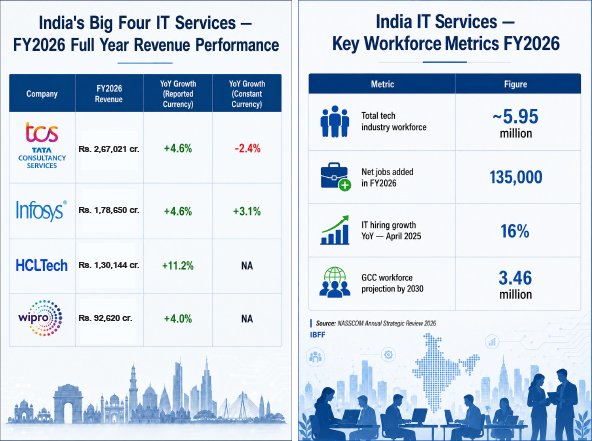

AI-related revenue across the total technology industry is estimated at $ 10–12 billion for FY26 — reflecting scaled, function-specific deployments moving beyond pilots into commercial offerings — according to NASSCOM. The industry added a net 135,000 jobs in FY26, taking total sector headcount across all sub-segments to nearly 5.95 million employees. April 2025 saw 16 percent YoY growth in hiring across the IT and BPM sector, driven by AI adoption, cloud modernisation, and GCC expansion, according to IBEF. Non-metro cities including Udaipur, Vizag, Coimbatore, and Nagpur recorded over 50 percent IT hiring growth in H1 2025 — significantly outpacing Bengaluru and NCR at 12–15 percent — reflecting a structural decentralisation of India's IT geography.

Global IT services spending grew 5 percent in 2025 and is projected to grow 5.2 percent in 2026, according to IDC projections cited in NASSCOM's Quarterly Industry Review — with India's growth running meaningfully ahead of the global average across all four measures.

The GCC story continued to be a defining structural feature of the Indian IT landscape in FY2025–26. India housed over 1,750 Global Capability Centres at the start of the fiscal year, with more than 150 new GCCs launched in the preceding 30 months. GCC salaries running 15–20 percent above traditional IT services rates are creating talent competition and wage pressure across the ecosystem — but GCCs are simultaneously validating India's talent depth and anchoring long-term enterprise commitment to the country. India's GCC workforce is projected to rise to 3.46 million by 2030, according to IBEF.

The AI Deflation Reality

The most significant and least anticipated development of FY2025–26 was what HCLTech CEO C. Vijayakumar called "AI deflation" in the company's FY26 earnings call in April 2026 — a phenomenon where AI-driven productivity improvements are compressing the revenue generated per unit of work, even as total deal volumes grow. TCS CEO K. Krithivasan described a similar dynamic, using the term "degrowth" to characterise certain service lines where AI automation has reduced the labour content of delivery. Infosys CEO Salil Parekh acknowledged deflation as an emerging factor while noting it had not yet materially impacted FY26 revenue, and Wipro CFO Aparna Iyer flagged lower margins in some AI-era deals.

The deflation dynamic operates as follows: a client that previously required 500 engineers to maintain an application estate may now require 200, with AI agents handling testing, monitoring, documentation, and first-level incident response. The deal still exists — and may even be larger by TCV — but the revenue per year is lower because fewer person-hours are being billed. For India's IT services industry, which built its scale on arbitrage between offshore labour costs and developed-market billing rates, AI deflation is a structural challenge that cannot be hedged through volume alone. The firms that will grow through it are those repositioning around outcomes, IP, and proprietary AI platforms rather than around headcount.

Key Players: FY2026 Performance

India's IT services industry in FY2025–26 was defined by diverging revenue trajectories among the top five players — with HCLTech outperforming the peer group, Infosys and Wipro delivering modest growth, and TCS facing a constant-currency revenue decline for the first time in its history as a listed company.

Tata Consultancy Services (TCS) reported consolidated revenues of $ 30 billion for FY2026 — the first time the company has crossed the $ 30 billion annual revenue milestone — with reported currency revenue up 4.6 percent YoY to Rs 2,67,021 crore, according to TCS's Q4 FY26 results announced on April 9, 2026. However, in constant currency terms, revenue declined 2.4 percent — reflecting continued softness in global discretionary IT spending and the AI deflation impact on certain service lines. Net profit for FY26 stood at Rs 49,210 crore, up 1.3 percent YoY. In a significant positive, TCS's annualised AI revenue crossed $ 2.3 billion in Q4 FY26 — a figure that demonstrates the company's growing AI services commercial traction. TCS ended FY26 with a headcount of 5,84,519 employees and total deal wins of $ 39.4 billion for FY25 — the strongest deal pipeline in its history. The company also announced a final dividend of Rs 31 per equity share for FY26.

Infosys reported FY26 revenues of $ 20,158 million — crossing the $ 20 billion annual revenue mark for the first time — with reported currency growth of 4.6 percent YoY and constant currency growth of 3.1 percent, according to Infosys's Q4 FY26 results announced April 23, 2026. Operating margin for FY26 was 20.3 percent (adjusted: 21.0 percent). Large deal TCV wins for FY26 totalled $ 14.9 billion — up 28 percent from the prior year — with net new business at 55 percent of total TCV. Free cash flow generation was strong at $ 3,733 million. CEO Salil Parekh attributed the performance to the "robustness of our enterprise AI value proposition and market share gains in large transformation opportunities." Infosys guided FY27 revenue growth at 1.5–3.5 percent in constant currency, with operating margin maintained at 20–22 percent.

HCL Technologies was the standout performer among India's top IT services firms in FY2026, with annual revenue growing 11.2 percent in reported currency terms — the strongest growth rate among the Big Four for the fiscal year — and headcount rising approximately 2 percent YoY. HCLTech's outperformance was driven by strong traction in BFSI and hi-tech verticals, positive seasonality in its software products business, and AI-led productivity improvements that supported margin expansion. Total deal TCV for the year was approximately $ 9.27 billion. However, CEO C. Vijayakumar cautioned that AI deflation is expected to reduce revenue by 3–5 percent in FY27 — a candid acknowledgment that the productivity gains currently helping margins will eventually compress top-line growth.

Wipro reported annual revenue growth of 4 percent in FY2026, with Q4 FY26 revenue of Rs 22,504 crore, up 1.33 percent YoY, according to results announced April 16, 2026. CFO Aparna Iyer pointed to lower margins in some AI-era deals and emphasised the need for continued operational improvement. Wipro guided FY27 revenue growth at negative 3.5 percent to negative 1.5 percent in constant currency — the most cautious guidance among the Big Four — reflecting client budget pressures and the ongoing transition in delivery economics. Total deal wins for FY25 stood at $ 3.95 billion.

Tech Mahindra guided FY26 constant currency revenue growth of 2–5 percent, with Q4 FY26 revenue of Rs 30,246 crore, up 6.13 percent YoY. The company has been executing a multi-year transformation under CEO Mohit Joshi, focusing on margin recovery, account mining, and AI capability development. Tech Mahindra's deal TCV for FY25 was $ 11.6 billion — second only to TCS among the Big Five.

Persistent Systems continued to outperform the industry, maintaining consistent double-digit revenue growth through FY2026, driven by its cloud-native, AI-services, and digital engineering focus. The company has become the benchmark for mid-tier IT services growth in India.

The Deals That Defined the Year

Several landmark deals and partnerships defined the commercial character of India's IT services industry in FY2025–26.

Infosys secured a $ 1.6 billion contract with the UK's NHS Business Services Authority in October 2025 — one of the largest public sector IT services deals in UK history — with AI and cloud transformation at its core. The company also secured a multi-year contract with a leading European financial services firm for end-to-end application modernisation using its AI-first delivery platform.

TCS signed a strategic partnership with four global IT majors — Cognizant, Infosys, Wipro, and itself — in the Microsoft Copilot enterprise deployment announced in December 2025, with each firm committing over 50,000 Copilot licences — the largest enterprise AI platform adoption globally. TCS also confirmed OpenAI as the first customer of its HyperVault AI data centre subsidiary, with an initial 100 MW capacity commitment scalable to 1 GW.

Wipro established a dedicated Microsoft Innovation Hub at its Bengaluru partner labs in December 2025, upskilling 25,000 employees in Microsoft Cloud and GitHub technologies as part of its AI-first delivery transformation. The company also expanded its partnership with Capgemini to deliver joint AI transformation programmes across European enterprise accounts.

HCLTech deepened its strategic partnership with Google Cloud in fiscal 2025–26, deploying Gemini Enterprise across enterprise client workflows, and signed a landmark deal with a leading US pharmaceutical company for AI-driven drug discovery and clinical data management platform development.

GCCs: The Parallel Economy Within IT Services

Global Capability Centres have emerged as a structurally important parallel to the traditional IT services export model — and in some dimensions, a competitive threat to it. India housed over 1,750 GCCs at the start of FY2025–26, with combined revenue estimated at $ 64.6 billion and a workforce of 1.9 million — numbers that rival the traditional IT services export model in both scale and sophistication. GCCs are no longer back-office extensions of global enterprises — they are becoming autonomous innovation hubs, running AI development, product engineering, cybersecurity operations, and financial modelling at global standards.

The GCC expansion has significant channel and ecosystem implications. Indian IT services firms are responding by positioning themselves as GCC setup, advisory, and managed services partners — helping global enterprises design, build, and operate capability centres in India. Firms including Nasscom, Tata Consultancy Services, and Infosys have formalised dedicated GCC advisory practices, recognising that the GCC economy will be a persistent and growing feature of India's IT landscape regardless of the traditional services export model's trajectory.

The Road Ahead: AI-First or Fall Behind

India's IT services industry enters fiscal 2026–27 with a clear strategic imperative: the firms that have built proprietary AI platforms, retrained delivery workforces, and repositioned around outcomes rather than headcount will grow. Those that have not will face deflation headwinds with no structural offset.

NASSCOM projects India's total technology industry to sustain 6–8 percent annual revenue growth through FY28, driven by AI services, engineering R&D, GCC expansion, and sovereign cloud infrastructure deployments. IDC projects global IT services spending to grow 5.2 percent in 2026 — providing an external demand tailwind even as per-unit revenue faces compression from AI deflation. The sector's total headcount of 5.95 million — with 135,000 net additions in FY26 — reflects continued employment growth, but the nature of that employment is changing. AI skills, platform engineering, and outcome-based delivery are the new currency of the Indian IT services talent market.

The total Indian technology industry crossed $ 300 billion in FY2025–26 — a genuine milestone. IT services exports, its largest component at over 65 percent of total technology exports, drove that achievement. Whether the next milestone — $ 500 billion — arrives on the back of intelligent services or in spite of AI deflation is the question that will define the industry's next decade.