Fiscal 2025–26 delivered record performances across PCs, servers and storage, while the AI compute wave reshaped enterprise infrastructure priorities and the printer segment held its ground through a shifting digital landscape

India's IT hardware market in fiscal 2025–26 was defined by two parallel stories unfolding simultaneously. On one side, the personal computing segment delivered its strongest year on record, fuelled by enterprise refresh cycles, consumer demand recovery, and the arrival of AI-enabled devices. On the other, the server and storage segments were reshaped by an AI infrastructure buildout of unprecedented scale, as hyperscalers and enterprises raced to deploy compute capable of handling generative AI workloads. Together, these stories reflect an IT hardware market in structural transformation — one that is no longer driven primarily by replacement cycles, but by the intelligence requirements of a digitally accelerating economy.

Personal Computers and Laptops

- A Record Year for India's PC Market

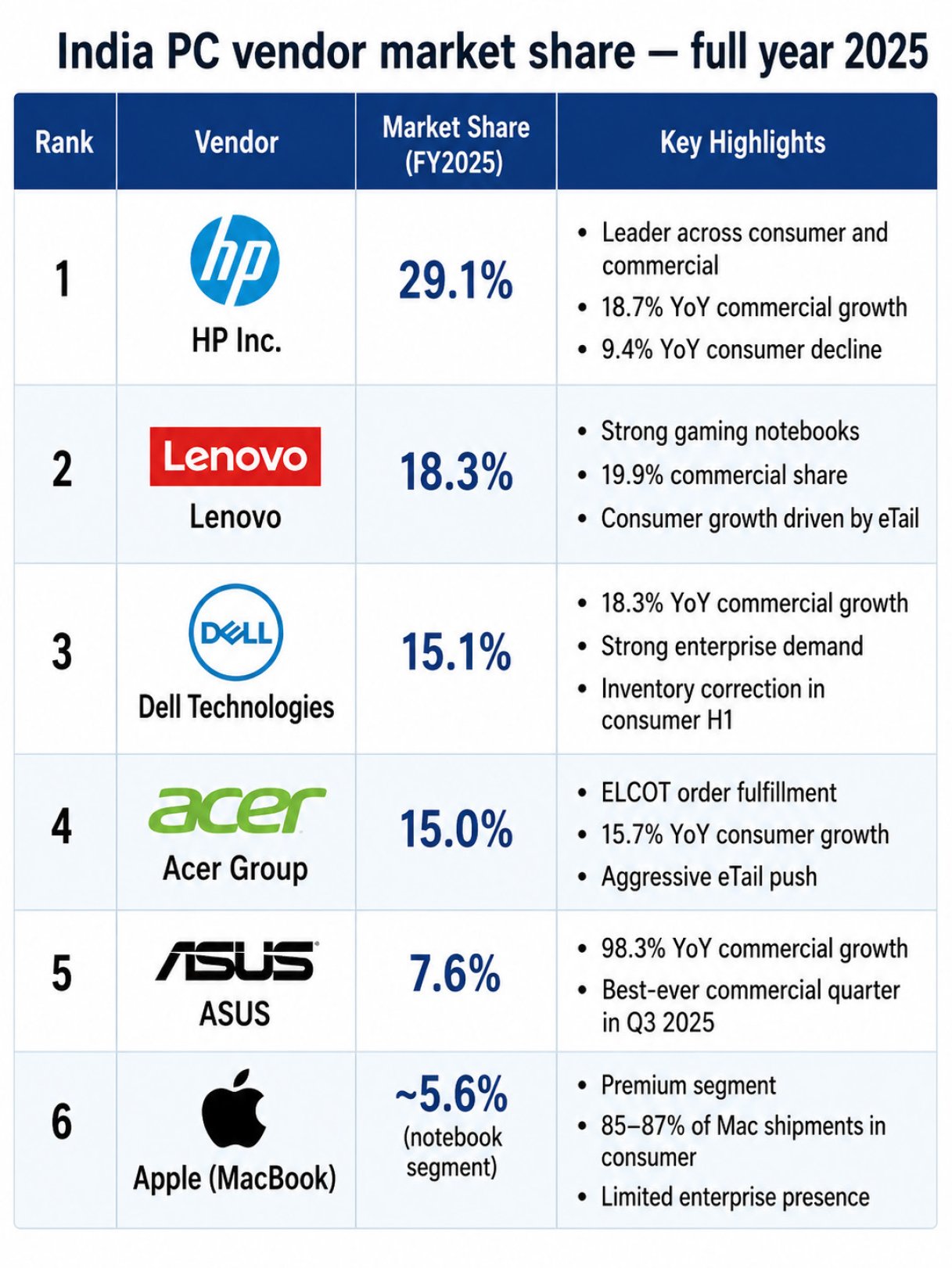

India's traditional PC market — encompassing desktops, notebooks, and workstations — recorded its strongest year in history in 2025, shipping 15.9 million units, growing 10.2 percent year-over-year, according to market research firm IDC. This marks the first time annual shipments have crossed the 15-million-unit milestone, surpassing the pandemic-driven peaks of 2021 and 2022. India's share of global PC shipments rose to 5.6 percent in 2025, up from 3.3 percent in 2020, reflecting the country's growing importance as a PC consumption market.

The market delivered strong momentum across all four quarters. Q3 2025 set a record with 4.9 million units shipped, growing 10.1 percent YoY, before Q4 2025 followed with 4.1 million units at 18.5 percent YoY growth — demonstrating sustained demand acceleration through the year.

By category:

Notebooks remained the dominant and fastest-growing form factor, expanding 12.4 percent YoY for the full year 2025. Desktops posted moderate gains of 3.6 percent YoY. Workstations emerged as the standout category, growing 24.2 percent YoY, driven by demand from data science, design, and AI-assisted content creation use cases. - Enterprise vs Consumer:

Commercial buyers accounted for 52.9 percent of PC shipments in India in 2025, with consumer at 47.1 percent. Enterprise demand was driven in significant part by the Windows 10 end-of-support deadline in October 2025, which accelerated fleet refresh decisions. SMB demand grew 18.8 percent YoY in Q3 2025, reflecting small business digitisation momentum. On the consumer side, PC shipments grew for the second consecutive year, driven by gaming, content creation, and virtual learning adoption. - AI PCs: AI-enabled notebooks sustained sharp growth throughout the year, surging 145.2 percent YoY in H1 2025. Basic AI notebooks — hardware-accelerated, entry-level AI devices — accounted for 88.1 percent of total AI notebook shipments in H1 2025. In Q3 2025, next-generation AI notebooks crossed the 100,000-unit shipment mark for the first time in a single quarter in India, signalling early enterprise adoption of higher-capability AI compute at the device layer.

Outlook:

IDC flagged rising component costs — particularly DDR RAM, GPUs, and processors — as significant headwinds for 2026. Despite strong underlying demand, affordability pressures from component inflation may moderate growth compared to the record 2025 performance.

Servers

- India's Server Market Accelerates on AI and Data Centre Buildout

India's server market was valued at $ 1.68 billion in 2025 and is projected to reach $ 3.36 billion by 2031 at a CAGR of 12.01 percent, according to Research and Markets. Demand was driven by the rapid expansion of hyperscale data centres — with Microsoft, Google, AWS, and domestic players including TCS HyperVault, Yotta, CtrlS, and Sify all scaling compute infrastructure significantly in fiscal 2025–26 — alongside strong enterprise adoption of AI and cloud-first architectures, and the government's IndiaAI Mission GPU procurement programme which awarded over 34,371 GPUs across two tender rounds in 2025.

Globally, the server market reached a record $ 112.4 billion in revenue in Q3 2025 alone, growing 61 percent YoY, according to IDC. Full-year 2025 global server revenue is projected at approximately $ 366 billion — up 45 percent over 2024 — driven by GPU-equipped AI server deployments, which accounted for more than half of total server revenue for the first time.

India's server market growth rate of over 25 percent annually outpaces the global average, reflecting the country's data centre buildout velocity and the structural effect of data localisation mandates requiring domestic server deployments for regulated workloads.

India-specific vendor market share data for servers is not publicly available from primary research firms. The key players active in India's enterprise and data centre server market in fiscal 2025–26, based on company announcements and industry coverage, were as follows: - Dell Technologies expanded its India enterprise footprint through its PowerEdge AI-ready server portfolio, with tight NVIDIA GPU integration, and deepened partnerships with Indian IT services firms deploying enterprise AI infrastructure across banking, telecom, and government verticals. Dell's server and networking segment globally hit $ 6.3 billion in Q2 2025, up 16 percent YoY, supported by strong demand for AI-ready systems.

- HPE was among the active vendors in India's enterprise server market across BFSI, government, and IT/ITES sectors through its ProLiant and Synergy portfolios, with AI accelerator integration delivered via its GreenLake managed services platform. In November 2025, HPE launched the Cray GX5000 supercomputing platform, designed for AI and HPC workloads — directly relevant to India's expanding AI research and enterprise compute requirements. HPE also introduced AI-driven networking and hybrid cloud infrastructure solutions at HPE Discover Barcelona in June 2025.

- Lenovo actively targeted the mid-market and SMB server segments in India through its ThinkSystem V4 server line — powered by Intel Xeon 6 processors optimised for AI and high-performance applications — which was available across the fiscal year. Lenovo's Data Center Group posted strong growth globally through 2025, and the company maintained an active presence in India's tier-2 data centre and enterprise segments.

- IBM focused on mission-critical deployments for banking and insurance in India, leveraging its Power10 server line for core banking modernisation and AI inference workloads. IBM's focus on hybrid cloud and AI-specific infrastructure made it a relevant option for India's largest financial institutions.

- Netweb Technologies, VVDN Technologies, and Consistent Infosystems represent the domestic Indian server manufacturing layer, building on PLI-enabled ODM models to reduce import dependence and participate in government and sovereign cloud procurement — a segment that is growing as public sector buyers prioritise Indian-origin hardware.

Storage

- Flash Dominates as AI Workloads Reshape India's Storage Market

India's data centre storage market was valued at $ 2.90 billion in 2025 and is projected to reach $ 3.51 billion in 2026 and $ 11.05 billion by 2032 at a CAGR of 21.12 percent, according to Mordor Intelligence. The structural shift toward All Flash Arrays is the dominant market trend — AFAs accounted for 38.10 percent of India's data centre storage market in 2025 and are growing at a 17.05 percent CAGR through 2032, as enterprises replace legacy spinning-disk infrastructure with flash platforms capable of supporting AI training, inference, and real-time analytics workloads.

Storage Area Networks retained the largest segment share at 45.40 percent in 2025, driven by BFSI and telecom platforms that require block-level throughput and low latency for mission-critical databases and payment processing. Network Attached Storage is the fastest-growing deployment type, with an 18.97 percent CAGR projected through 2032, fuelled by analytics, media production, and hybrid cloud data workflows.

Globally, the external enterprise storage systems market grew 2.1 percent YoY in Q3 2025 to $ 8.0 billion, according to IDC — a more modest trajectory than servers, but with All Flash Arrays growing 17.6 percent YoY as AI adoption accelerates demand for high-performance flash. IDC projects full-year 2025 ESS market growth at 5.5 percent, extending to 6.3 percent in 2026.

India-specific vendor market share data for storage is not publicly available from primary research firms. The key players active in India's enterprise storage market in fiscal 2025–26 were: - Dell Technologies (through PowerStore, PowerMax, and PowerScale portfolios) was active across enterprise storage deployments, particularly in large IT services firms, banking, and government data centres. Globally, Dell recorded a 22.7 percent revenue share in external enterprise storage in Q3 2025, according to IDC — the highest among tracked vendors — though India-specific share figures are not publicly available.

- NetApp was active in enterprise NAS and AFA deployments across India's BFSI, IT/ITES, and government sectors. Its ONTAP platform is widely deployed in hybrid cloud environments, and its all-flash array performance drove solid global growth — 2.8 percent YoY revenue growth in Q3 2025 — as Indian enterprises prioritised flash migration for analytics workloads. NetApp and QNAP both expanded multiprotocol access and scale-out NAS capabilities relevant for India's media and analytics verticals.

- Pure Storage expanded its India presence through FlashArray and FlashBlade platforms, targeting analytics and AI workloads. Pure delivered double-digit global revenue growth in Q3 2025, driven by AI and neocloud demand that is directly mirrored in India's expanding AI infrastructure buildout.

- HPE Alletra addressed mid-market enterprise storage requirements under the GreenLake consumption model. Samsung appointed Acro Engineering as its national SSD distributor in India in August 2025, expanding Gen 4 and Gen 5 SSD availability — a move that signals growing enterprise and data centre appetite for high-performance solid-state storage at scale.

Printers

- A Resilient Market Anchored by Ink-Tank Adoption and Government Demand

India's printer market demonstrated continued resilience in fiscal 2025–26, sustaining demand through strong SME, government, education, and healthcare procurement despite the broader shift toward paperless workflows. The India printer market is projected to reach $ 2.49 billion by 2026, according to Fortune Business Insights, supported by MSME digitisation programmes, compliance documentation requirements, and a structural shift from cartridge-based to ink-tank devices that has broadened the addressable buyer base.

Globally, the printer market was valued at $ 55.63 billion in 2025 and is expected to reach $ 78.64 billion by 2033 at a CAGR of 4.42 percent, according to IMARC Group, with Asia Pacific holding the largest regional share at 44.7 percent in 2025. In India, ink-tank printers continued to gain market share at the expense of traditional cartridge devices, driven by total cost of ownership advantages — particularly relevant for SMEs and home offices. Multi-function devices held 40.61 percent of India's inkjet printer market in 2025, reflecting demand from hybrid working environments. Laser printers maintained their position in enterprise and government bulk printing, while the government's sustained effort to curb the reconditioned copier market continued to drive original laser device demand.

According to IDC's Worldwide Quarterly Hardcopy Peripherals Tracker, globally HP Inc. led printer shipments with a 34.2 percent unit share in Q4 2024, followed by Epson at 22.5 percent, Canon at 20.4 percent, and Brother at 9.8 percent. India-specific printer market share data is not published separately by IDC. The key players and their India performance in fiscal 2025–26 were: - HP Inc. maintained market leadership in India across both consumer and enterprise printer segments. In February 2026, HP launched a new DeskJet All-in-One range in India designed specifically for home users, students, and small offices — featuring plug-and-play functionality, dual-band WiFi, and models built with at least 70 percent post-consumer recycled plastic. In March 2026, HP introduced a new LaserJet portfolio with quantum-resistant security features, AI-powered document scanning — delivering 50 percent faster scan-to-email workflows — and enhanced duplex printing speeds targeting SMB productivity requirements.

- Canon India expanded its production printing portfolio in July 2025, launching an upgraded imagePRESS V1000 with a new Vacuum Paper Feeding Deck at Print Expo Chennai 2025. The upgraded system, designed for light and mid-production print environments, supports uninterrupted print runs of up to 10,000 sheets and is compatible with the existing imagePRESS V900/V800/V700 series — extending the installed base value for existing Canon customers. Canon also showcased upgraded wide format imagePROGRAF printers at the same event, targeting construction, design, and manufacturing verticals.

- Epson India made its most significant India-specific commitment of the fiscal year in July 2025, opening India's first high-capacity ink tank inkjet printer manufacturing facility within the factory of partner RIKUN Manufacturing Pvt. Ltd. in Chennai, with mass production commencing in October 2025. The facility is part of Epson's broader localisation strategy for India — a market where over 8 million EcoTank units have been sold since 2010. In June 2025, Epson also launched the EcoTank L4360, a compact Wi-Fi multifunction printer targeting home offices and small businesses.

- Brother India focused on the SMB and SOHO segments with a wide service network, maintaining relevance in the mid-market through competitively priced multifunction laser devices. Ricoh India and Konica Minolta India competed in the enterprise MFP and managed print services segments, targeting document workflow integration with large enterprise and government clients.

India's printer market faces a structural tension between digital substitution and sustained physical documentation requirements in education, government, healthcare, and MSME segments. The ink-tank transition remains the dominant product trend — vendors without a credible ink-tank portfolio will continue to lose share to Epson and Canon. Cloud-connected printing, AI-enhanced document scanning, and managed print services are the primary value-add layers for enterprise channel partners in fiscal 2026–27.

Make in India: PLI Drives Domestic Manufacturing

India's Production Linked Incentive Scheme 2.0 for IT hardware — covering laptops, tablets, all-in-one PCs, servers, and ultra-small form factor devices — delivered measurable results in fiscal 2025–26. The scheme, launched in May 2023 with a budgetary outlay of Rs 17,000 crore, had already driven Rs 10,000 crore in production and created 3,900 direct jobs within its first 18 months of operation, according to DD News citing government data. Twenty-seven companies including Dell, HP, Acer, Asus, Lenovo, Foxconn, Flextronics, VVDN, and Syrma SGS are approved under the scheme, with production underway across manufacturing units in Chennai, Noida, and Bengaluru. Over its full tenure, PLI 2.0 is projected to generate Rs 3.5 lakh crore in total production and 47,000 jobs. For the channel ecosystem, domestic manufacturing translates directly into shorter supply chains, reduced import dependency, and greater pricing stability — particularly relevant given global component cost volatility in fiscal 2025–26.

The Road Ahead

India's IT hardware market enters fiscal 2026–27 with strong momentum but clearly differentiated trajectories across segments. The PC market faces component cost headwinds after a record year, with DDR RAM, GPU, and processor price inflation likely to moderate shipment growth. Servers will continue their AI-driven hypergrowth as India's data centre buildout accelerates toward the government's 9 GW capacity target by 2030. Storage will consolidate around flash platforms as AI and analytics workloads displace legacy spinning-disk. Printers will sustain steady growth anchored by ink-tank adoption, government procurement, and managed print services in enterprise.

Across all segments, the common thread is intelligence — AI PCs, AI servers, flash storage optimised for AI inference, and AI-enhanced printing and document workflows. India's IT hardware market is not simply growing. It is evolving toward a new infrastructure layer for the intelligent enterprise.