The era of lift-and-shift is over. India's cloud story in 2025–26 is about sovereignty, AI-native infrastructure, and an unprecedented wave of global capital betting on the subcontinent's digital future

There was a time not long ago when cloud adoption in India was measured primarily by the number of enterprises moving workloads off ageing on-premise hardware and onto rented servers somewhere in Mumbai or Singapore. The conversation was dominated by cost savings, uptime guarantees, and cautious IT managers convincing CFOs that the public cloud was, in fact, secure. Fiscal 2025–26 rendered that conversation obsolete. The questions Indian enterprises are asking today are fundamentally different: Which cloud platform can run our AI agents at scale? Where does our regulated data live, and who governs it? Can we build a sovereign cloud that does not depend on infrastructure we do not own? These are not the concerns of early adopters — they are the strategic preoccupations of a market that has grown up fast, and is now writing the next chapter on its own terms.

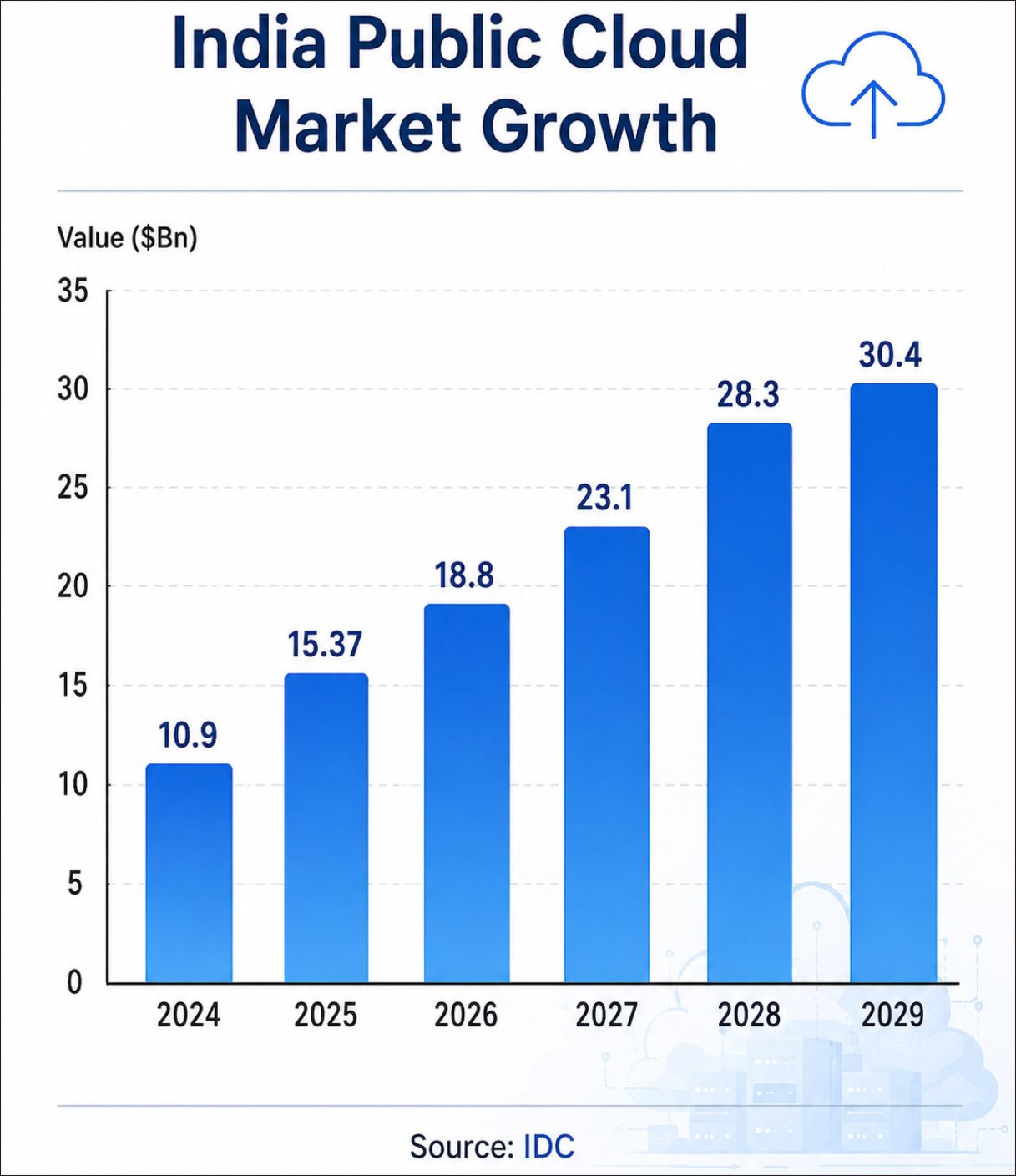

India's Cloud Market: Size, Speed, and Structural Shift India's public cloud services market, covering IaaS, PaaS, and SaaS, generated $ 10.9 billion in revenue in 2024, according to IDC's Worldwide Semi-annual Public Cloud Services Tracker. IDC projects the market to reach $ 30.4 billion by 2029, growing at a CAGR of 22.6 percent over 2024–29, with AI adoption identified as the primary catalyst. Statista's 2025 estimate for India's public cloud market puts the current-year figure at $ 15.37 billion, reflecting the sharp acceleration in AI-driven cloud spending through the year. NASSCOM, in its landmark report "Future of Cloud and Its Economic Impact: Opportunity for India," projects cloud technology to contribute 8 percent of India's GDP by 2026 — a 4x increase from its earlier contribution — and estimates the sector's potential to create 14 million jobs.

India's public cloud services market, covering IaaS, PaaS, and SaaS, generated $ 10.9 billion in revenue in 2024, according to IDC's Worldwide Semi-annual Public Cloud Services Tracker. IDC projects the market to reach $ 30.4 billion by 2029, growing at a CAGR of 22.6 percent over 2024–29, with AI adoption identified as the primary catalyst. Statista's 2025 estimate for India's public cloud market puts the current-year figure at $ 15.37 billion, reflecting the sharp acceleration in AI-driven cloud spending through the year. NASSCOM, in its landmark report "Future of Cloud and Its Economic Impact: Opportunity for India," projects cloud technology to contribute 8 percent of India's GDP by 2026 — a 4x increase from its earlier contribution — and estimates the sector's potential to create 14 million jobs.

The composition of demand is evolving rapidly. IaaS is the largest segment by infrastructure spend, driven by enterprises seeking scalable compute without heavy capital investment. SaaS remains the most widely adopted service category, used by over 84 percent of large Indian organisations, per NASSCOM data. BFSI holds the largest industry-specific share, reflecting the sector's deep dependence on cloud for core banking, fraud analytics, and real-time payments infrastructure. Healthcare is emerging as the fastest-growing vertical, driven by telemedicine expansion, AI diagnostics, and digital health records mandates.

The hybrid cloud model is gaining strong traction as enterprises seek to balance public cloud agility with the data residency requirements imposed by the Digital Personal Data Protection Act, 2023, and RBI-specific data localisation mandates.

The Hyperscaler Bet: $67.5 Billion in Commitments

Between October and December 2025, Amazon, Microsoft, and Google collectively pledged $ 67.5 billion in Indian investments — 80 percent of which were announced in December alone, according to The Washington Post. It was, by any measure, the largest concentration of global technology capital ever directed at India in a single period.

Microsoft fired the opening salvo in December 2025, when CEO Satya Nadella announced a $ 17.5 billion investment in cloud and AI infrastructure, skilling, and operations in India, to be deployed between 2026 and 2029. The investment — the largest single technology commitment in Asia's history — will scale up existing cloud infrastructure in Chennai, Hyderabad, and Pune, and bring online a new Azure data centre region in Hyderabad, comprising three availability zones, in mid-2026. Microsoft is offering sovereign public and sovereign private cloud services across multiple Indian regions. Tarun Pathak, Research Director at Counterpoint Research, said at the time that the investment gave Microsoft a "first-mover advantage in GPU-rich data centres while making Azure the preferred platform for India's AI workloads."

Amazon Web Services, which already controls an estimated 40 percent of India's cloud services market and has invested $ 3.7 billion in Indian data centres historically, announced plans to invest an additional $ 8.3 billion in Maharashtra to expand cloud infrastructure through 2030. Google announced plans to invest $ 15 billion in building a gigawatt-scale AI and cloud hub in Visakhapatnam, southern India. Separately, Google and Reliance unveiled a dedicated cloud region in Jamnagar, further deepening the search giant's local infrastructure footprint.

Key Players: IT Giants, Indian Cloud Builders, and the Channel Ecosystem India's cloud story has multiple protagonists, and a Brand Book that serves the channel ecosystem must account for all of them — from the large IT services integrators to the homegrown cloud and data centre operators who form the backbone of enterprise and government cloud infrastructure across the country.

India's cloud story has multiple protagonists, and a Brand Book that serves the channel ecosystem must account for all of them — from the large IT services integrators to the homegrown cloud and data centre operators who form the backbone of enterprise and government cloud infrastructure across the country.

Among the IT services majors, TCS was named a Leader in the IDC MarketScape for Asia-Pacific Professional and Managed Services for Google Cloud in March 2026. Infosys embedded cloud and AI capabilities across its delivery lines, focusing on a "human plus agent" operating model for global enterprise clients. HCL Technologies deepened its Google Cloud partnership, deploying Gemini Enterprise across workflows. Wipro established a Microsoft Innovation Hub at its Bengaluru partner labs and upskilled 25,000 employees in Microsoft Cloud and GitHub technologies. Persistent Systems continued to record strong growth as enterprises sought cloud-native architecture depth rather than legacy-migration experience.

However, it is India's homegrown cloud and data centre operators who deserve particular recognition in fiscal 2025–26, as they moved from the periphery of the cloud story to its centre — handling sovereign workloads, competing for hyperscale contracts, and expanding aggressively across tier-2 and tier-3 geographies.

CtrlS Datacenters, one of India's largest Tier-4 certified data centre and cloud operators, committed $ 2 billion for expansion across green, AI-ready campuses. In January 2025, it signed an MoU with the Telangana government to develop a 400 MW data centre cluster, inaugurated its Chennai data centre campus with an investment of approximately $ 482 million, and launched its Kolkata DC1 facility. CtrlS was among the Indian firms approached by OpenAI in September 2025 for preliminary discussions on hosting capacity for its global Stargate infrastructure project.

ESDS Software Solution, the Nashik-based cloud and data centre provider, posted a landmark fiscal 2024–25, with total revenues rising 27 percent year-on-year from Rs 287 crore to Rs 361 crore, and international revenues surging 600 percent. ESDS's eNlight Cloud — India's first cloud computing platform to be patented in both the US and UK — offers real-time auto-scaling of CPU and RAM without downtime. ESDS serves public sector entities across smart cities, e-governance, and sector-specific digital initiatives, and is preparing for an IPO that reflects growing investor confidence in India-native cloud innovation.

NxtGen Infinite Datacenter continued to distinguish itself as a high-density, AI-ready cloud provider, offering Nvidia H100 and H200 and AMD MI300X GPUs to support India's AI compute requirements. NxtGen is an active partner in the government's IndiaAI Mission and signed a $ 27 million contract with Akash Systems for advanced Diamond Cooling servers.

Yotta Data Services (Hiranandani Group) pivoted decisively from traditional colocation to becoming an AI cloud powerhouse, procuring 16,000 Nvidia H100 GPUs for its Shakti Cloud with plans to scale to 32,768 units. Yotta's NM1 facility in Navi Mumbai remains Asia's largest Tier-4 certified data centre. Like CtrlS, Yotta was also part of OpenAI's preliminary Stargate discussions in India.

Sify Technologies, one of India's earliest cloud pioneers and operator of six Tier-3 data centres across major cities, continued to serve large enterprise and government clients with colocation, managed hosting, and cloud migration services, backed by one of India's largest private network backbones.

E2E Networks, listed on the National Stock Exchange, carved out a distinct position as India's leading GPU cloud provider for AI workloads — serving startups, researchers, and enterprises that require accelerated compute at Indian data residency.

Cyfuture Cloud rounded out the competitive domestic field with MeitY-approved, PCI DSS and ISO 27001 certified data centres, an end-to-end AI cloud built and operated entirely in India, and a broad GPU portfolio serving enterprises, government agencies, and startups across the AI compute spectrum.

Together, these homegrown operators represent a maturing domestic cloud industry that is no longer merely complementary to the hyperscalers — it is, in several sovereign and regulated segments, the preferred and mandated choice.

The Road Ahead: AI-Native, Sovereign, and Hybrid

The Indian cloud market's next phase will be shaped by three converging forces. First, the AI-native transition — enterprises are no longer procuring cloud as infrastructure alone; they are buying cloud as the platform on which AI agents, foundation models, and real-time inference workloads run. Every major hyperscaler is now competing as much on its AI platform capabilities — Amazon Bedrock, Azure AI Foundry, Google Vertex AI — as on raw infrastructure pricing.

Second, sovereign and hybrid cloud will become the default architecture for regulated sectors. The BFSI, healthcare, and government verticals — which together represent the largest share of India's cloud spend — will increasingly demand domestic data residency as a baseline, not a premium.

Third, the channel ecosystem will be central to translating hyperscaler capital commitments into enterprise outcomes. The billions committed by AWS, Microsoft, and Google are being deployed through a dense network of Indian cloud partners — system integrators, managed service providers, and cloud-native consultancies — whose capacity to architect, implement, and govern complex cloud environments will determine whether India's cloud ambition converts to measurable enterprise value.